Knowing the differences between Medicare Supplements F, G, and N will help you determine if supplemental coverage is right for you. Photo by Storyblocks.

What is Medicare and Why Do People Need Medicare Supplements?

Medicare is a federal health insurance program primarily designed for Americans aged 65 and older. While some younger individuals qualify due to disability, the program mainly serves those transitioning into retirement, ensuring they have access to affordable healthcare. Original Medicare covers essential medical services like hospital stays, doctor visits, preventive screenings, and durable medical equipment. However, it doesn’t cover everything—leaving enrollees responsible for deductibles, copays, and coinsurance. That’s where Medicare Supplements (also called Medigap plans) come in! These plans help reduce out-of-pocket costs, making healthcare more accessible and predictable for retirees.

How Do Medicare Supplements Work?

As the name suggests, Medicare Supplements work alongside Original Medicare, helping to cover costs that Medicare alone doesn’t pay for. Private insurance companies offer these plans, but the federal government standardizes them. This scenario means the benefits for each plan remain the same no matter which insurer you choose. The main difference? Pricing.

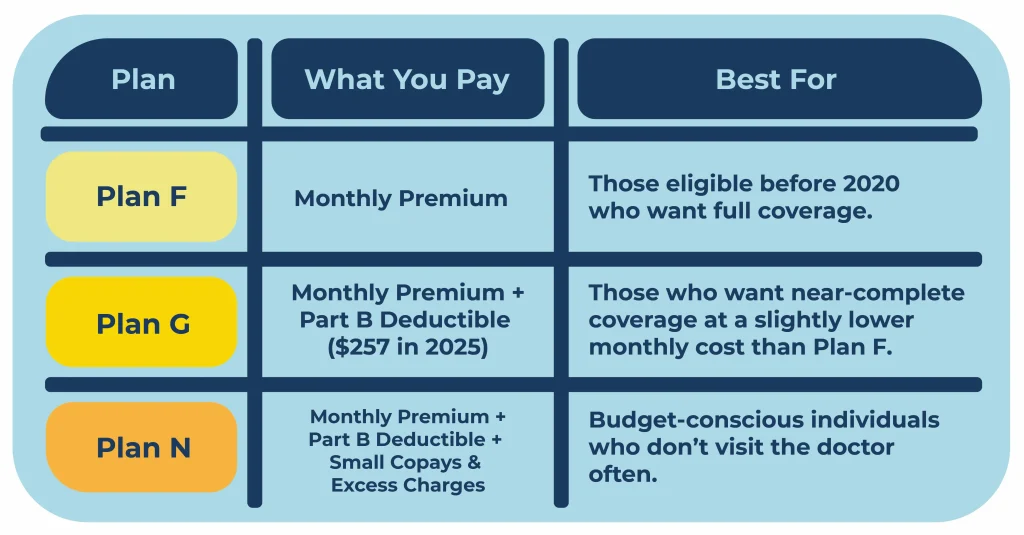

There are ten Medicare Supplement plans, each labeled with a letter. However, as of 2025, Plans F, G, and N are the most popular choices. Let’s break them down!

Plan F: The Cover-All

Plan F is known as the most comprehensive Medicare Supplement because it covers everything except your monthly premium. Here’s what it pays for:

- Medicare Part A coinsurance and hospital costs

- Hospice care coinsurance and copays

- Medicare Part B coinsurance and copays

- Medicare Part A and B deductibles

- Emergency medical care while traveling abroad

- First three pints of blood for transfusions

With Plan F, you’ll never have to worry about unexpected medical bills—just your monthly premium.

Important Note: Plan F is only available to those who qualified for Medicare before January 1, 2020. If you become eligible after that date, Plan F is not an option for you.

Plan G: The Next Best Thing

Plan G is nearly identical to Plan F, with one key difference: it does not cover the Medicare Part B deductible. That means it covers:

- Medicare Part A coinsurance and hospital costs

- Hospice care coinsurance and copays

- Medicare Part B coinsurance and copays

- Medicare Part A deductible

- Emergency medical care while traveling abroad

- First three pints of blood for transfusions

BUT

- You will pay the Part B deductible out of pocket (a one-time cost of $257 in 2025.)

For those who aren’t eligible for Plan F or want a more affordable premium, Plan G is often the best alternative.

Plan N: The Budget-Friendly Choice

If you’re looking to lower your monthly premiums and don’t mind paying a little more out-of-pocket for doctor and hospital visits, Plan N could be a great fit. It covers:

- Medicare Part A coinsurance and hospital costs

- Hospice care coinsurance and copays

- Medicare Part B coinsurance (except for some copays)

- Medicare Part A deductible

- Emergency care abroad

However, unlike Plans F and G, Plan F requires:

- A $20 copay per doctor’s visit

- A $50 copay per ER visit (will be waived if admitted)

- You will pay excess charges if your physician is not participating in Medicare assignment

Plan N is perfect for healthy individuals who don’t visit the doctor often and want to save on premiums.

How to Choose the Right Plan for You

Here’s a simple breakdown to help you decide which plan is the best fit for you.

Takeaway

The best Medicare Supplement for you depends on your needs and budget. Want full coverage with no surprise costs? Plan F is your best bet (if eligible). Would you prefer a lower premium and don’t mind covering the Part B deductible? Plan G is a solid choice. Are you looking to save even more and don’t visit the doctor often? Plan N could be the perfect fit.

Medicare needs can change, so it’s always wise to assess and reassess your options. For personalized guidance, we recommend connecting with a licensed Medicare expert.

Got Medicare Questions?

We hope that this information on Medicare Supplements was useful to you.

Let us help you answer your questions so that you can get back to the activities that you enjoy the most.

Call (888) 446-9157, click here to get an INSTANT QUOTE, or leave a comment below!

See our other websites: